Top 5 Ways To Get Fast And Easy Loans In Canada

Running out of money is a natural occurrence for the average Canadian individual, and while it's an unwanted scenario, it happens. This misfortune can be the result of employment loss, medical bills, emergencies, slow cash flow, and more.

Nevertheless, going through the lengthy process of acquiring conventional loans may be impossible, especially when you have no collateral or even a poor credit score. Fortunately, several methods exist for Ontario residents and throughout Canada that provide quick and easy loans for you during such a financial emergency.

This article will guide you through the top five ways to get quick and easy loans in Canada even when you have no assets to pledge as collateral. Read on!

1. Payday Loans

Payday loans are common types of personal loans for individuals looking for quick access to cash either during emergencies, before their next paycheck, or for other reasons. While Payday loans typically have high-interest rates, they are unsecured loans, meaning they require no collateral before entering your bank account.

Furthermore, borrowers are required to repay this loan within their next payday, usually within two weeks, which is realistic for the small amount these lenders offer. Essentially, most payday loans give out a loan amount up to $1,500 to limit the risk the financial institution incurs without collateral; nevertheless, online payday loans are quick loans that are perfect for a dire financial situation.

How do Payday Loans work?

Borrowers can acquire a payday loan in Canada by either applying online or visiting a brick-and-mortar. After receiving your details, these financial businesses will perform a thorough assessment of your credit score.

However, it's worth noting that some payday loan companies offer emergency funds with no credit check; nevertheless, the company will always demand proof of income and your pay date to ensure you're capable of repaying.

Payday Loan Repayment

The repayment process of any loan is crucial, and payday loans typically give two weeks to return the borrowed funds. Alternatively, you can give the lender a postdated check to deposit on your payday.

Another way to repay a payday loan is by granting the lender access to funds in your account, allowing them to make money once you receive money from your employer, social benefits, or pension.

Borrowing Fees and Costs

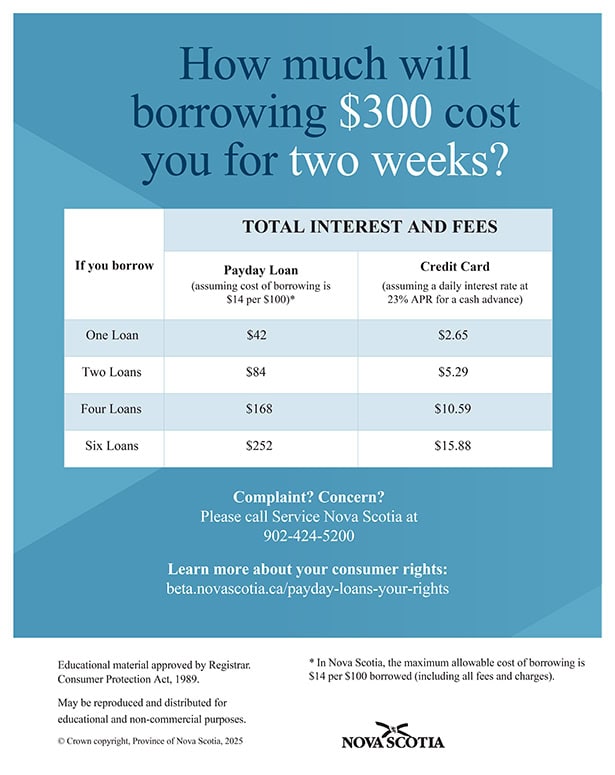

Typically, Payday loan interest rates in Canada are unlike traditional types as they are calculated based on the amount you borrow. In other words, these companies set payday feeds ranging from $10 to $30 for every $100 borrowed.

Therefore, a payday loan of $15 per $100 is an annual percentage rate (APR) of almost 400 percent, which is enormous compared to the 12 percent to about 30 percent APRs on credit cards.

Note that some loan companies offer a "Rollover" whenever you're unable to repay the loan at the expected time. The rollover allows you to pay the initial borrowing fee until your next paycheck arrives; however, you're still hooked to the original loan balance alongside the fee for the rollover, thereby increasing the total repayment amount.

*Note: laws exist that limit lenders from giving interest rates above 30%; however, payday lenders fall under exemptions that allow for such maximum charges.

Pros and Cons of Payday Loans

Like every source of emergency funds, this type of loan come with their benefits and disadvantages. These include:

Pros

-

Easy to access

-

Fewer requirements than secured loans

-

(bad credit loans) Accessible to people with low credit

-

Requires no collateral

-

Quick loan application process

Cons

-

Steep borrowing costs (high cost loans)

-

Higher chances of getting trapped in a debt cycle

-

They don't help you build credit

2. Personal Line of Credit

Line of Credit is another reliable method for acquiring quick cash for residents of Ontario and throughout Canada as it works similarly to a credit card gotten from the bank. Essentially, this method allows you to borrow money up to a preset limit and you only repay the precise amount you borrowed.

Naturally, this means of collecting emergency funds is known as an unsecured loan, meaning that no collateral is required. Unlike payday loans, Lines of Credit loans come with a low-interest rate typically less than 10% alongside zero fees with a same-day deposit.

How Line of Credit Loans Works

Traditional secured loans require you to pay interest on the lump sum immediately after receiving it, and this requirement is necessary irrespective of when you use the money.

For a Line of Credit, you're granted access to a specific amount of money that you can withdraw whenever you need. Unlike traditional loans, you're not required to pay this given amount until you borrow from the preset amount allocated to you.

It's also worth mentioning that having a great credit score helps with receiving a lower annual percentage rate. Regardless, expect most Line of Credit loans to have annual fees and limits on how much you can withdraw.

Upon qualifying for the Line of Credit, the bank will give you a set time frame to collect money from the account called the "Draw period", which lasts several years. There will be a special card or check dedicated to using and transferring money whenever necessary.

Difference Between Credit Card and Line of Credit

Line of Credit and Credit Cards seem similar since you can withdraw money from both with a preset limit, repay with interest, and borrow again. However, these financial methods are two different products offered by lenders.

Essentially, Credit Cards don't have a draw period, allowing you to use the product as long as the account stays open. In fact, many Credit cards come with reward programs that let you avoid paying interest if you repay withdrawn money on time monthly.

Furthermore, Credit Cards typically have higher interest rates than Lines of Credit; however, they offer lower financial limits.

Line of Credit Repayment

Upon receiving a personal Line of Credit, you will be given a period where you can withdraw funds, known as the "Draw Period". If you still have unpaid withdrawals after this Draw Period ends, you will automatically enter a repayment phase.

Different types of repayments exist and how you cover any remaining balance depends on the method the lender chooses. The options include:

Demand Line of Credit

This method grants lenders the legal right to demand full payment at any time; fortunately, it's not common for lenders to set up Personal Lines of Credit as a Demand Line of Credit.

Balloon Payments

The balloon payment method requires borrowers to pay the full balance once the draw period ends.

Draw and Repayment Periods

The repayment period is the most common option lenders use when creating a Personal Line of Credit. It requires borrowers to make monthly payments during the repayment period.

These different repayment periods may be tricky to comprehend on your first day; therefore, we recommend taking time to understand the lender's terms and develop a repayment plan as well.

Pros and Cons of Line of Credit

A personal Line of Credit is an excellent choice for individuals seeking fast-cash and short-term loans; however, understanding its pros and cons allows you to determine whether it's perfect for you.

The perks and disadvantages of a Line of Credit include:

Pros

-

Doesn't require a collateral

-

Quick access to cash

-

Only pay interest on the money you withdraw

-

Better interest rates than Credit Cards

-

Overdraft protection (some accounts)

Cons

-

Unstable interest rate

-

Interest isn't tax-deductible

-

Ideal for people with a good credit score

3. Credit Cards

Credit cards are a common option for emergency and everyday funds, giving borrowers money whenever necessary. What makes this form of borrowing unique is that users won't pay any interest if they repay their balance on time, allowing them to borrow money for free.

Suppose you fail to pay the balance on time, Credit Card companies are legally required to give borrowers 21 days of grace period before interest on expenses begins to accrue.

How Credit Cards Work

Credit cards are issued by financial institutions with a credit limit that dictates how much you can spend on services and goods. In simple terms, credit cards allow you to borrow cash quickly and replay later.

Like many services, the way your credit card works is dependent on the rules and regulations set by the financial institution. Therefore, it's best to read the terms and conditions documents as it contains interest rates, loan limits, and fees.

It's also worth emphasizing that credit cards report your repayment history to two credit bureaus in Canada, which are Equifax and TransUnion. So, using your credit card and repaying withdrawals on time can improve your credit score, making you eligible for more or other loan types in the future.

Credit Card Loan Repayment

Credit card loan repayments are amongst the easiest to perform as statements are issued at the end of each billing cycle. This monthly review showcases transactions and the balance owed, giving you a clear picture of your financial responsibility.

You can opt between paying the minimum payment, full balance, or something in between the lowest and maximum amount. However, it's worth noting that choosing the minimum or partial payment can result in interest charges that can add up quickly and increase your overall payment.

Credit Card Interest Rates

Credit Card users are required to pay an interest rate alongside the money borrowed from the bank. This interest is called the annual percentage rate, or APR, and can range from 10% to 20% in Canada.

Note that some financial institutions give borrowers an interest-free grace period for purchases, which lasts around 21 days. This period begins on the last day of your billing cycle, protecting you from owing interest before pushing your balance.

Pros and Cons of Credit Cards

Credit cards are a financially convenient way to get emergency cash or cover expenses before your next paycheck. In fact, Canada currently has 76.2 million credit cards in circulation, meaning the majority of Canadians have two of these cards.

Before choosing this method, here are some pros and cons to consider:

Pros

-

Fast cash for emergencies

-

Builds your credit score

-

Rewards for quick repayments

Cons

-

Overspending created more debt

4. Peer-to-Peer Lending

If you're unwilling to go through traditional banks or get a payday loan either due to bad credit or no collateral, an alternative method of financing would be Peer-to-Peer Lending. In simple terms, Peer-to-Peer Lending is where one person lends money to another individual directly.

This method gained popularity with people seeing alternative lending options, spawning several websites dedicated to connecting borrowers with lenders.

How Peer-to-Peer Lending Works

Peer-to-Peer Lending, also known as P2P Lending, happens today when borrowers meet lenders or investors online to fund a loan partly or completely. First, people looking for a loan must read the terms and conditions of the investor, determining whether they can get a better deal from the bank.

Note that these investors will determine the interest rate, repayment period, and more, which will also depend on other income, credit history, and other factors. You can capitalize on this method by finding a P2P lending platform, creating an account, verifying your identity, then dropping a request for financial support.

Eventually, an investor or more will contact you, and provide their terms and conditions. Once all parties reach an agreement, you'll receive your money via Email money transfer, your bank, or other means provided.

Peer-to-peer Lending in Canada

Despite being well-established in the United States, P2P lending isn't popular in Canada; nevertheless, the lending method is present in the country and has increased in popularity recently.

In fact, Canadian regulations allow P2P lending companies and platforms to offer 24/7 service to Canadians. This liberty has created popular establishments like goPeer and Lending Loop, opening new ways for borrowers to receive funds often within 24 hours of requesting.

Pros and Cons of Peer-to-Peer Lending

Peer-to-Peer Lending is a wholesome concept as strangers unite to aid other strangers in need. Naturally, it's best to consider the pros and cons before opting for this method. These include:

Pros

-

Potentially provided both long and short-term loans

-

Access to fast loans with a quick application

-

Lower interest rates compared to traditional options

-

No fees if you repay the loan on time

Cons

-

Most platforms reject people with a low credit score

-

Fewer regulations can lead to unsafe practices

-

Additional fees when creating an account like finder's fee and loan origination

5. Family and Friends

Lastly, one of the most reliable ways to find emergency cash during a job change or before your next paycheck is with family and friends. Essentially you've already built Social Capital with these close ones, making it easier to get their assistance irrespective of your credit score.

Furthermore, the repayment process with family and friends is flexible as you can pick the most ideal repayment schedule with little to no interest.

However, it's worth emphasizing that while borrowing money from family and friends is effective, it has also permanently damaged relationships. This issue is due to little or no repayments of the loan, resulting in regret and a depreciation of your respect.

Therefore, only employ this method if you're certain of your ability to repay the loan on time and respect the lender in the process; otherwise, use the previous options.

Conclusion

It's not uncommon to experience financial difficulties at any stage in your life, especially now that sectors are still recovering from the Covid-19 pandemic. Therefore, we recommend using any of the options listed in this article as they all provide emergency funds within 48 hours.

However, ensure your needs are urgent and your finances are capable of handling the debt before choosing these same-day loan options; else, you hurt your credit and be unable to repay the debt.