Why we need payday lenders

Over the years we have heard some alarming statistics about payday lenders, more precisely payday loan shops--like how payday lending is correlated with property crime, violence, increased premature mortality, and the increased need for social assistance.

Payday loan shops themselves are not the cause of these issues, they are simply part of a wider social challenge that small-short term loan customers are facing.

In trying to resolve this social challenge, provinces have tightened the legislation surrounding those small short-term loans. Loan fees that lenders can charge went down significantly over the past two years and new legislation is also providing customers with more flexibility to repay their loan. The traditional payday loan we used to know no longer exist as it has evolved into a completely different financial product.

This new approach is far better than simply banning payday loans as this would have created an even bigger problem. If a person cannot get cash through a regulated payday lender, they are bond to go to a loan shark or another worse alternative (such as an unregulated online lender). For this reason, banning payday loans simply wasn’t the solution.

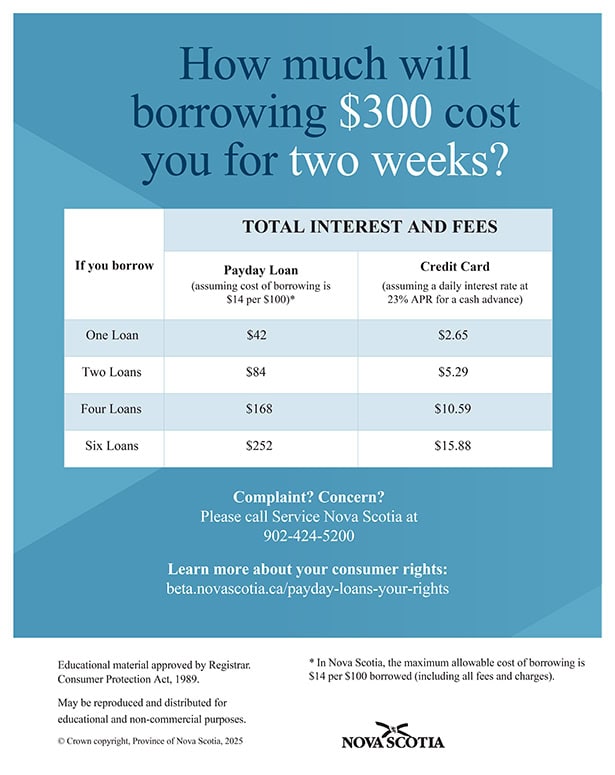

Analyzing the cost associated with services charged by Banks and other service providers we quickly understand why payday loans are necessary. Small short-term loans cost a lot less than the late fees and non-sufficient fund fees the consumers may face otherwise.

The legislators have taken the right approach. This financial product will continue to evolve and as more businesses enter the market, new products and more alternatives will be available to help these customers obtain short-term credit at reasonable cost.